Understanding Payment Fees: From Cost Centre to Revenue Stream (Part 1)

Willem Pino

Engineering

Your PSP invoice is likely a major hidden cost, but you can turn it into a growth lever.

In this first post of a two-part series, you'll learn how to understand payment processing costs and effectively evaluate PSP pricing.

In Part 2, we’ll shift focus from cost control to revenue growth. We will show you how platforms can monetise payments, dynamically manage fees, and drive margins through smart pricing strategies.

Inside pricing for a PSP: Interchange and Scheme Fees

Cards and alternative or bank-based payment methods have distinctly different cost structures. The latter typically operate under a single buy rate, the base cost charged by the payment method itself. This is a flat fee or percentage. For cards, this is more complicated. Your PSP pays both interchange and scheme fees.

Interchange fees are paid to the cardholder’s bank

Scheme fees are charged by the Card Network like Visa or Mastercard.

Understanding these can help you lower your costs.

The interchange rate applied to a transaction depends on multiple variables, including:

Card type: the underlying product on the card which can be a consumer card, or a commercial card (e.g., business or corporate cards).

Funding source: the underlying source that used to pay (e.g., debit or credit funding sources)

Checkout channel: the channel that is used to convert a sale (e.g. online or an in-person payment).

Regionality: a variable determined by where the cardholder’s bank is located and where the transaction is accepted (e.g. an US cardholder shopping at an NL website).

Markets like the EEA regulate interchange rates, limiting costs for certain transactions.

Scheme fees, on the other hand, relate more directly to the transaction's journey. Each step in the lifecycle of a card transaction can trigger a different scheme fee. For example:

Using 3DS will incur a specific scheme fee.

Allowing a customer to check out in a foreign currency may result in another.

The rate of these scheme fees is typically influenced by the same variables that determine interchange, including card type, usage environment, and regionality.

How Your PSP’s Costs Translate to Your Pricing

|  |

Your pricing mirrors the PSP’s costs:

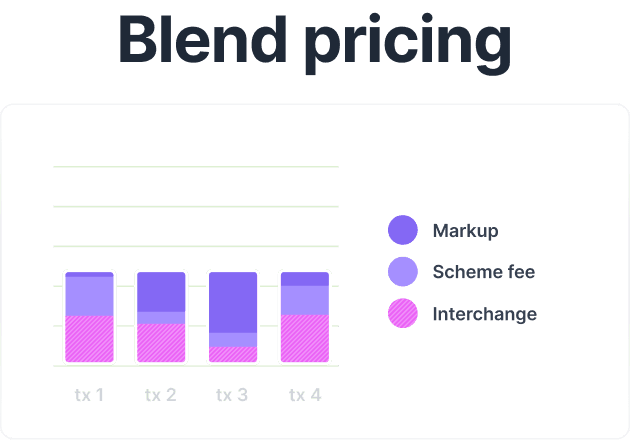

Blended pricing offers a flat or percentage rate per transaction, typical for alternative and bank-based methods. For cards, this means the same pricing no matter the card type.

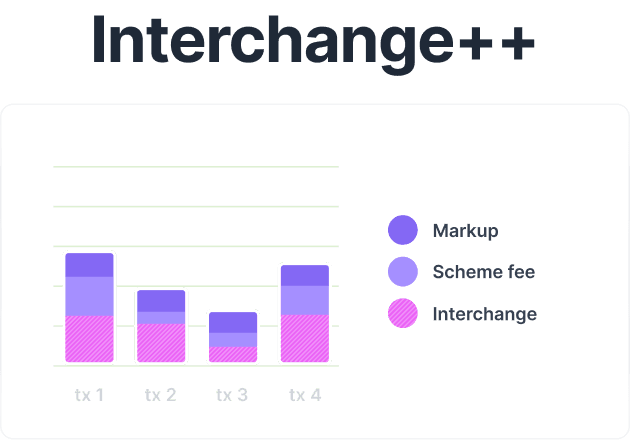

Interchange++ pricing passes on the interchange and scheme fees, plus a mark-up: the Payment Service Provider’s fee for facilitating the transaction.

This is the sell rate of the PSP. The margin is either the sell rate minus the buy rate, or in the case of interchange++, the mark-up. The margin covers their operational costs and risk.

If you opt for a blended pricing model for your card volume, your provider still pays interchange++ behind the scenes, it’s simply wrapped into the blended rate you see. Bundling makes it harder to identify actual costs and spot overpayments.

Blended vs. Interchange++: Which Fits Your Business?

Interchange++ pricing can seem complex at first. Blended pricing is simpler but often includes an extra buffer, particularly if you process low-cost domestic debit cards.

Many markets regulate interchange for certain card types. Europe does so under the Interchange Fee Regulation introduced in 2015. As a rule of thumb, consumer cards are priced at 0.20% for Debit and 0.30% for Credit. Some countries within Europe have even stricter rules, such as the Netherlands that has set the interchange at 0.02 EUR fixed for consumer debit cards issued in the Netherlands, or Belgium that charges 0.10% (with a cap of 0.05 EUR) on consumer debit cards issued in Belgium.

As a general guideline:

Choose blended pricing if:

You prefer simplicity over detailed cost management.

You want to avoid fee volatility, which might affect the predictability of your margin when you resell payments under a blend.

You manage to negotiate a single blend rate for your total card mix, which has the potential to be cheaper if you process a lot of international and commercial cards. Although PSPs are likely aware of this or have clauses to revise pricing.

Choose interchange++ if:

You handle high volumes and want to minimize costs.

You value transparency and control over your costs.

You process a significant number of regulated domestic debit cards, especially in markets like the Netherlands or Belgium, where interchange rates are very low.

You can request a fee simulation from your payment provider or do an analysis yourself to get a sense of what your underlying interchange and scheme fees will be. This will help you understand which model best matches your card mix and volumes.

Additional Fees That Impact Your Margins

The transaction rate is just one component. Watch out for other fees that impact margins:

Setup Fees: Some providers charge a fee just to get started which sometimes is called an integration fee. A provider that is easy to integrate to rarely has fees like this.

Refund and Chargeback Fees: Refunds and chargebacks have a cost price, but evaluate these fees closely. You might be overpaying on them, especially when you operate in a high volume and/or high-risk vertical.

Monthly Account Minimums: In some cases when you negotiate a price with your Payment Service Provider, they ask for a monthly minimum amount or a commitment. It is common to have this in place, but it can be difficult to reach your minimums if you have a multi-processor setup.

Optimizing Payment Costs with Tiered Pricing

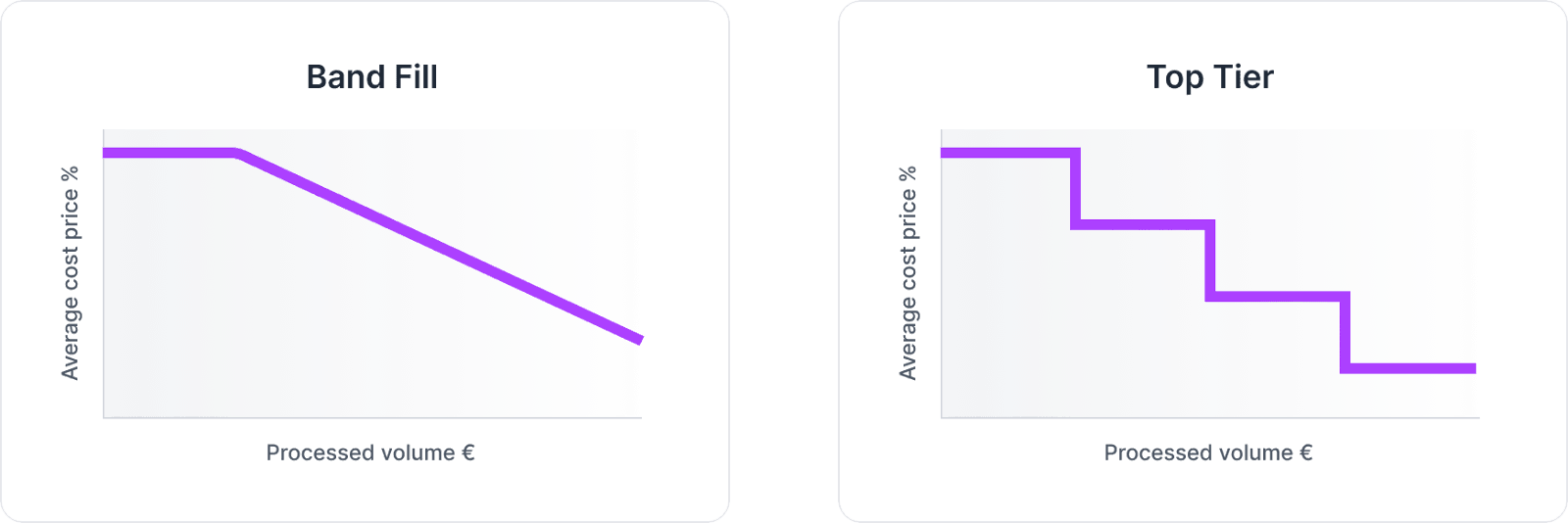

If you expect strong growth in payment volume, consider negotiating a top-tier pricing model. Under this model, once you reach a specific volume tier, the rate for that tier applies to your entire transaction volume, not just the portion within that tier. This is different from band-fill pricing, where only the volume within each tier benefits from the corresponding rate.

Example:

Let’s say your monthly volume is €1,000,000 and the pricing tiers are:

Tier 1: 2.0% for the first €500,000

Tier 2: 1.8% for the next €500,000

Tier 3: 1.6% above €1,000,000With band-fill pricing, you would pay:

2.0% on the first €500,000 → €10,000

1.8% on the next €500,000 → €9,000

Total: €19,000 → Effective rate: 1.9%

With top-tier pricing, once you reach €1,000,000, the Tier 2 rate of 1.8% would apply to the full amount, resulting in:

1.8% on €1,000,000 → €18,000

Effective rate: 1.8%

Top-tier pricing starts higher but delivers greater savings as volume scales. If you’re confident in fast growth, the long-term savings can be significant.

Also pay attention to how the tiers are applied. Some providers apply pricing at the individual merchant level, which fragments your volume and prevents you from accessing better rates. Negotiate for tiering to be applied on your aggregate platform volume, using your full scale to your advantage.

Always model growth scenarios to find the best pricing structure for your business stage.

Transparent Pricing, Real Partnership

At Rootline, we believe transparency is the foundation of a strong payment strategy. Our clear interchange++ pricing, combined with detailed transaction-level reporting that breaks down every cost component at the transaction level, ensures you can trace every fee directly back to the original transaction. You have full control and visibility over your payment costs.

Whether you're launching or scaling your platform, we work closely with you to embed cost efficiency and operational clarity into your payments infrastructure from day one. We don't just process transactions, we help you build your business.

In the next part of this series, we’ll explore how payments can transition from a cost center to a powerful revenue driver, highlighting how Rootline equips your platform with the tools to do so.

Want to optimize your payments strategy? Schedule a call with Rootline.

Want to learn more?

Explore Rootline in more detail or speak to our team to see how it can support your platform.